U.S. Default, Growing Inequality, & "Transitory" Inflation: Pt. 1

U.S. Default, Growing Inequality, & "Transitory" Inflation: Pt. 1

Part 1: U.S. Default/Debt Ceiling Propaganda & Growing Inequality

Intro

Policymakers are at it again. Except, they’re no longer kicking the can down the road. This time, they’re attempting to kick a box of broken glass bottles uphill, while barefoot, with thousands of people beneath them, desperately clinging on with both hands. If policymakers are successful in their latest attempt, the subsequent momentum from the downfall will have massive repercussions for Americans.

In their latest attempt at papering over the U.S.’s growing sovereign debt crisis, the talk of the town is how catastrophic a default or failure to lift the debt ceiling would be amidst a plethora of other real issues. In our first ever write-up, we’ll break this down into three parts. We’ll first crush any assertion that defaulting or failing to raise the debt ceiling would be a negative, let alone catastrophic. Next, we’ll reveal the destructive nature of the Federal Reserve’s misleading inflationary policies, which will continue hitting the lower and middle classes the hardest. Lastly, we’ll offer up a simple, alternative solution proving that these officials are either clueless or corrupt, while giving our prediction for the most likely outcome, and finally, ways we look to protect our wealth.

Our purpose of writing this is to show the public that their concerns about the market and their financial situations are warranted. We believe the public has been lied to countless times and there’s no better time to acknowledge reality. We hope to shed light on the unpopular truth and give our readers an alternative perspective that may better resonate with their real-world experiences. While the truth may be frustrating, we hope you find this useful.

Propaganda

In the latest round of Washington propaganda, big business CEOs were invited to brief the President on our looming financial crisis1. All appearing to read off of a pre-written script, executives joined Biden in public videoconferences to give their latest pleas that a default would be catastrophic. JPMorgan’s CEO Jamie Dimon claimed there are huge economic costs already being borne. Jane Fraser of Citi (former recipient2 of multi-trillion dollar backdoor bailout) said defaulting is going to cause lasting damage to the credibility of the United States. Keep in mind that JPMorgan and Citi are both required to hold HQLAs (high-quality liquid assets) such as Treasury securities per post-Financial Crisis regulation Basel III3. This gives the big banks a glaring conflict of interest, since a default could result in lower bond prices, crushing the banks’ assets.

Nasdaq’s CEO Adena Friedman said financial markets would react very, very negatively. Others may find it quite humorous that Raytheon’s CEO was also invited, considering the weapons supplier is one of the biggest beneficiaries of wars, paid for by the government’s endless debt issuance. No conflict of interest there. This is fearmongering centered around baseless claims from those who benefit the most from big government and more debt.

In a separate note, Moody’s, who so accurately predicted4 the worst financial crisis of our lifetimes (sarcasm), claims5 that a U.S. default would cost 6 million jobs, sending the unemployment rate from around 5% today to 9%. Finally! A concrete claim we can debate. Let’s first consider what our debt is being used for today. Over $5.3T in legislation6 has been enacted in response to Covid-19 so far, largely to continue paying individuals who are no longer working in the form of stimulus checks, unemployment benefits, rental assistance, etc. Keep in mind that politicians such as Nancy Pelosi, Andrew Yang, and Mitt Romney have been calling for UBI7 (universal basic income) for years, way before the pandemic. So, if our debt is being issued to pay people NOT to work, and people don’t need to work because they’re getting paid, what will happen with unemployment if debt is no longer issued to pay those people to NOT work? That’s right, kids! Unemployment would actually go DOWN. Again, this is a repeat of the old Great Financial Crisis scare tactics in telling everyday Americans that if we didn’t shell out trillions of taxpayer dollars to the big banks, then the ATMs would quit working.

Pre-Covid Economy

Do you do your own grocery shopping? Have you seen empty shelves recently, or perhaps, are the goods that remain 10, 20, or 30% more expensive? Is your favorite brand of cereal now offered in 16.9oz boxes vs. 20oz boxes just a year ago for the same price (“shrinkflation”)? While it’s easy to empathize with those affected by Covid-19, we must not ignore the implications of endless spending. The supply chain shortages are real and worsening8. Meanwhile, the U.S. now has more job openings than any time in history9. We’ll touch more on this topic in Part 2, but we, unlike the Federal Reserve who controls our money supply, don’t believe higher inflation is a good thing10. It’s pretty easy for the working class to see that government spending subsidizing those who aren’t producing is only going to hurt consumers amidst serious supply chain issues. Kamala Harris praises recent efforts to lift the debt ceiling11 while telling you that Christmas presents won’t be available12 due to supply chain shortages. How fucking stupid are these people? More importantly, how stupid do they think we are?

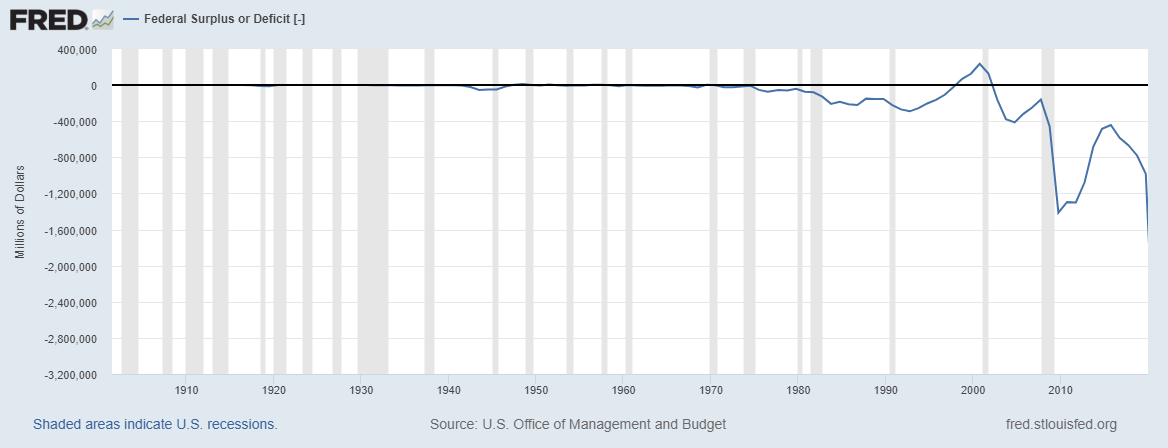

Let’s first consider what benefits, if any, have come from running a large fiscal deficit. The chart below shows our fiscal deficit growing to >$1.6T by the end of 2019. This is a good proxy since Covid-19 had zero financial implications in the U.S. at this point. What this means is that each year, the U.S. government spends $1.6 TRILLION more than it brings in through taxes.

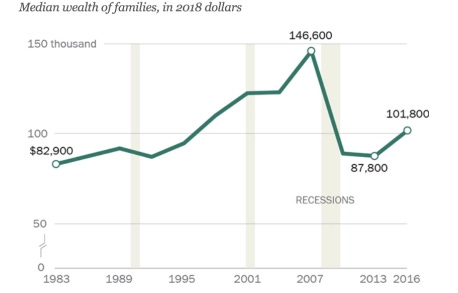

So, the $64 thousand question is how were Americans doing in 2019? Have increased deficits helped Americans along the way? The Economist reported13 in 2019 that soon-to-be retirees had a median 401(k) balance of just $21,000. After tax, that sounds like just one year’s worth of rent payments. Forget about food or healthcare. Older millennials (then ages 32-37) only had $1,000 in their 401(k)s. Forbes reported14 that a quarter of all Americans and 13% of those 60 or older had no retirement savings at all. Additionally, the Pew Research Center put out a report15 back in early 2020 showing that, adjusted for inflation, the median family net worth was at the same level as it was back in 1995.

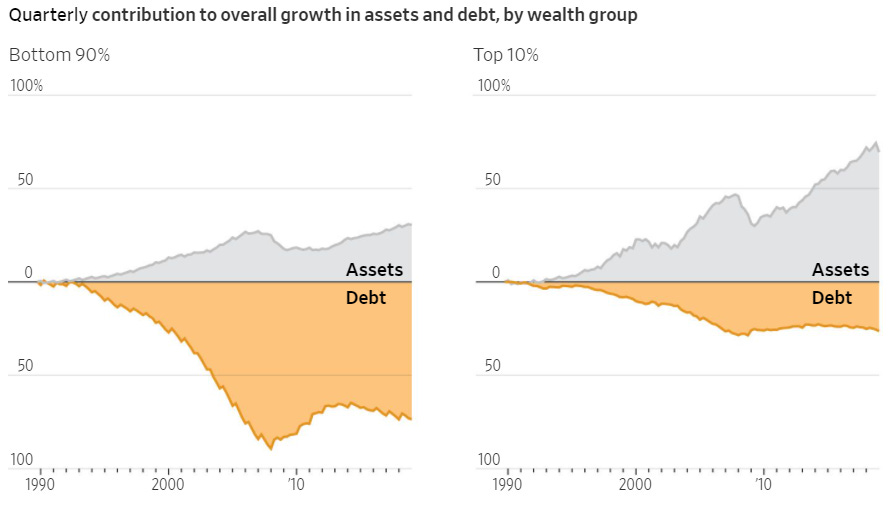

Politics aside, the economy was not sound under Obama or Trump. The Wall Street Journal put out a popular and lengthy piece back in 201916 talking about how families are going deeper in debt to just stay in the middle class. The authors did a nice job of highlighting the explosion in consumer debt such as student loans, auto debt, and credit cards. Their chart below shows how the ballooning debt has held back the bottom 90% as the top 10% thrive.

Growing Inequality

However, a common narrative you may hear is that debt doesn’t matter because interest rates are low. The article claims that despite the rising debt, consumers aren’t nearly as debt-burdened as they once were since the debt service to disposable income ratio was down to 9.9% from 13.2%. This is a horrible misconception used to excuse poor policy decisions that trap the bottom 90% in debt. Here’s how this works:

Lower interest rates are required to afford higher and higher debt loads

Lower interest rates discourage savings (no investment return) and encourage consumption

Saving less means a down payment on house is harder to afford for first-time buyers, which makes it more likely that someone would rent

Mortgage payments are part of debt service while rent is not

Therefore, under the authors’ assessment, those who spend all of their money and can’t afford to buy a house are better off than those who save and purchase a home where they can increase their net worth over time as they build equity

Meanwhile, those strapped with debt fall further and further behind

The government “comes to the rescue” with a new spending plan to “help” Americans

Circle back to point #1

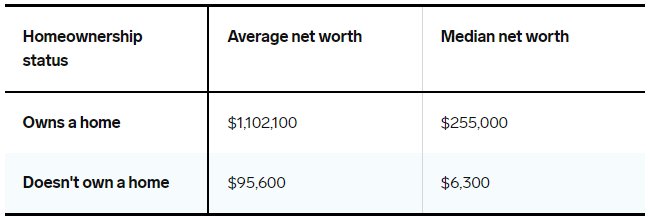

There are two Americas: The Haves (top 10%) and the Have Nots (bottom 90%). Those who owned a home though all of this debt spending (chart below17) have benefited greatly as lower and lower interest rates has made it more difficult to save.

The same can be said for those previously invested in stocks. Lower bond interest rates push investors into higher risk assets like equities, which have risen substantially and left the bottom 90% behind while the top 10% thrived.

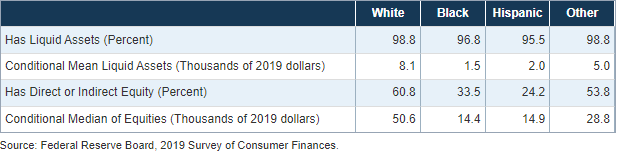

The Fed is now constantly talking about fighting racial inequality18 (a common fad nowadays), yet their policies that have lifted equity prices have exacerbated racial inequality as minorities hold fewer stocks and have lower home ownership rates. Don’t buy their bullshit. They could care less about minorities or the middle class.

To summarize, the U.S. government’s endless spending, and the Fed’s lower interest rate policies to help the government afford that spending, have crushed the real economy and fueled inequality. It’s no surprise that legislators have leveraged a pandemic to increase their spending powers. With that being said, their historical track record should give us pause as we consider new spending effectiveness. It’s been a massive failure thus far, and spending must be capped. In Part 2 we’ll tackle the highly inflationary effects of Covid-19 spending.

-MavInvest

https://www.yahoo.com/now/biden-meet-ceos-highlight-risk-120532815.html

https://wallstreetonparade.com/2015/03/warren-citigroup-morgan-stanley-merrill-lynch-received-6-trillion-backdoor-bailout-from-fed/

https://www.bis.org/publ/bcbs238.pdf

https://www.cbsnews.com/news/moodys-to-pay-864m-to-settle-claims-it-inflated-ratings-leading-up-to-financial-crisis/

https://www.washingtonpost.com/us-policy/2021/09/21/debt-ceiling-recession-/

https://www.pgpf.org/blog/2021/03/heres-everything-congress-has-done-to-respond-to-the-coronavirus-so-far

https://progressive.org/op-eds/guaranteed-basic-income-mccabe-200807/

https://www.theatlantic.com/ideas/archive/2021/10/america-is-choking-under-an-everything-shortage/620322/

https://www.nbcnews.com/business/business-news/u-s-now-has-more-job-openings-any-time-history-n1276367

https://www.cnbc.com/2020/05/11/central-banks-might-succeed-after-trying-for-a-decade-to-generate-inflation.html

https://www.local10.com/news/politics/2021/10/07/exclusive-interview-with-vice-president-kamala-harris/

https://www.foxnews.com/media/kamala-harris-christmas-shopping-leo-terrell

https://www.cnbc.com/2019/12/12/system-is-flawed-when-most-americans-have-tiny-retirement-savings.html

https://www.forbes.com/sites/niallmccarthy/2019/06/03/report-a-quarter-of-americans-have-no-retirement-savings-infographic/?sh=5e1b7c463ebf

https://www.pewresearch.org/social-trends/2020/01/09/trends-in-income-and-wealth-inequality/

https://www.wsj.com/articles/families-go-deep-in-debt-to-stay-in-the-middle-class-11564673734?mod=hp_listb_pos2

https://www.businessinsider.com/personal-finance/average-american-net-worth

https://www.bloomberg.com/features/2021-federal-reserve-race-inequality/?sref=0mbebkji